Gold Commodity Price Prediction Using Tree-based Prediction Models

Keywords:

Commodity Price, Gold, Machine Learning, Price Prediction, Tree-based ModelAbstract

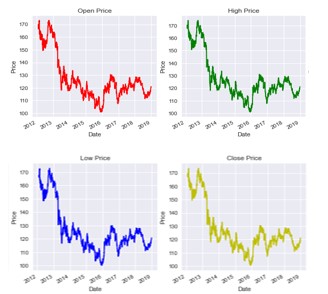

Commodity price forecasting is always a matter of research for practitioners and academia as a non-linear price structure of commodity with large volatility is associated with it. The efficiency of price prediction systems has been proven with the recent expansion of Artificial Intelligence and enhanced capabilities of computational equipment. Machine Learning (ML) is widely used in predicting the prices across the markets. Though a variety of ML methods are in use to predict commodity prices in recent times, this paper attempts to predict gold commodity closing prices specifically using tree-based models including Decision Tree, Adaptive Boosting (AdaBoost), Random Forest, Gradient Boosting, and eXtreme Gradient Boosting (XGBoost). The inputs to each of the prediction models were chosen from a total of nine technical indicators such as Simple 10-day moving average, Weighted 14-day moving average, Momentum, Stochastics K%, Stochastic D%, Relative Strength Index (RSI), William’s R%, Moving Average Convergence Divergence (MACD) and Commodity Channel Index (CCI) and four metrics namely RMSE, MAE, MSE and R2 were analysed for each technique of all the tree-based models considered and which were internally competing to explain superior forecast. All four metrics were calculated to check the effectiveness of different prediction models.

Downloads

References

A. Upadhyay, G. Bandyopadhyay, and A. Dutta, “Forecasting Stock Performance in Indian Market using Multinomial Logistic Regression”, Journal of Business Studies Quarterly, vol. 3, no. 3, pp. 16–39, 2012.

K. K. Sureshkumar and N. M. Elango, “An Efficient Approach to Forecast Indian Stock Market Price and their Performance Analysis”, International Journal of Computer Application, vol. 34, no. 5, 2011.

K. Miao, F. Chen, and Z. Zhao, “Stock price forecast based on bacterial colony RBF neural network”, Journal of Qingdao University, pp. 210–230, 2007.

E. S. Olivas, “Handbook of research on machine learning applications and trends: Algorithms, methods, and techniques”, IGI Global, 2009.

I. E. Livieris, E. Pintelas, and P. Pintelas, “A CNN-LSTM model for gold price time-series forecasting,” Neural computing and applications, vol. 32, pp. 17 351–17 360, 2020.

A. Liaw and M. Wiener, “Classification and regression by Random Forest”, Rnews, vol. 2, no. 3, pp. 18–22, 2002.

O. Elijah, L. A. Mckinnell, and A. W. V. Poole, “Neural network-based prediction techniques for global modeling of M(3000) F2 ionospheric parameter”, Advances in Space Research, vol. 39, no. 5, pp. 643–650, 2007.

H. Wei, Y. Nakamori, and S. Y. Wang, “Forecasting stock market movement direction with support vector machine,” Computers and Operations Research, vol. 32, no. 10, pp. 2513–2522, 2005.

M. Vijh, D. Chandola, V. A. Tikkiwal, and A. Kumar, “Stock closing price prediction using machine learning techniques,” Procedia computer science, vol. 167, pp. 599–606, 2020.

I. Parmar, N. Agarwal, S. Saxena, R. Arora, S. Gupta, H. Dhiman, and L. Chouhan, “Stock market prediction using machine learning,” proceedings of 2018 First International Conference on Secure Cyber Computing and Communication (ICSCCC), pp. 574–576, 2018.

V. K. S. Reddy, “Stock market prediction using machine learning,” International Research Journal of Engineering and Technology, vol. 5, no. 10, pp. 1033–1035, 2018.

M. Usmani, S. H. Adil, K. Raza, and S. S. A. Ali, “Stock market prediction using machine learning techniques,” proceedings of 2016 3rd International Conference on Computer and Information Sciences (ICCOINS), pp. 322–327, 2016.

M. Umer, M. Awais, and M. Muzammul, “Stock market prediction using machine learning (ML) algorithms”, Advances in Distributed Computing and Artificial Intelligence Journal, vol. 8, no. 4, pp. 97–116, 2019.

A. Moghar and M. Hamiche, “Stock market prediction using LSTM recurrent neural network”, Procedia Computer Science, vol. 170, pp. 1168–1173, 2020.

K. Pahwa and N. Agarwal, ““Stock market analysis using supervised machine learning,” proceedings of 2019 International Conference on Machine Learning, Big Data, pp. 197–200, 2019.

S. Ravikumar and P. Saraf, “Prediction of stock prices using machine learning (regression, classification) Algorithms”, proceedings of 2020 International Conference for Emerging Technology (INCET), pp. 1–5, 2020.

S. Mokhtari, K. K. Yen, and J. Liu, “Effectiveness of artificial intelligence in stock market prediction based on machine learning”, preprint arXiv:2107.01031 2021.

N. Naik and B. R. Mohan, “Optimal feature selection of technical indica- tor and stock prediction using machine learning technique,” proceedings of International Conference on Emerging Technologies in Computer Engineering, pp. 261–268, 2019.

M. Nikou, G. Mansourfar, and J. Bagherzadeh, “Stock price prediction using deep learning algorithm and its comparison with machine learning algorithms”, Intelligent Systems in Accounting,” Finance and Manage- ment, vol. 26, no. 4, pp. 164–174, 2019.

I. E. Livieris, E. Pintelas, and P. Pintelas, “A CNN-LSTM model for gold price time-series forecasting,” Neural computing and applications, vol. 32, pp. 17 351–17 360, 2020.

M. Hiransha, E. A. Gopalakrishnan, V. K. Menon, and K. P. Soman, “NSE stock market prediction using deep-learning models,” Procedia computer science, vol. 132, pp. 1351–1362, 2018.

R. Nandakumar, K. R. Uttamraj, R. Vishal, and Y. V. Lokeswari, “Stock price prediction using long short term memory,” International Research Journal of Engineering and Technology, vol. 5, no. 3, 2018.

M. Roondiwala, H. Patel, and S. Varma, “Predicting stock prices using LSTM”, International Journal of Science and Research, vol. 6, no. 4, pp. 1754–1756, 2017.

M. Nabipour, P. Nayyeri, H. Jabani, A. Mosavi, and E. Salwana, “Deep Learning for Stock Market Prediction”, Entropy, vol. 22, no. 8, 2020.

P. Sadorsky, “Forecasting solar stock prices using tree-based machine learning classification: How important are silver prices?” The North American Journal of Economics and Finance, vol. 61, pp. 101 705– 101 705, 2022.

Z. H. Kilimci, “Ensemble Regression-Based Gold Price (XAU/USD) Prediction”, Journal of Emerging Computer Technologies, vol. 2, no. 1, pp. 7–12, 2022.

J. S. Sevic and A. J. Stakic, “Prediction of Gold Price Movement Considering the Number of Infected with the Covid 19,” proceedings of International Scientific Conference on Information Technology and Data Related Research, 2022.

K. N. Devi and V. M. Bhaskaran, “Semantic enhanced social media sen- timents for stock market prediction,” International Journal of Economics and Management Engineering, vol. 9, no. 2, pp. 678–682, 2015.

M. Nabipour, P. Nayyeri, H. Jabani, and A. Mosavi, “Deep learning for Stock Market Prediction”, arXiv:2004.01497, 2020.

S. Mishra, D. Mishra, and G. H. Santra, “Adaptive boosting of weak regressors for forecasting of crop production considering climatic vari- ability: An empirical assessment”, Journal of King Saud University - Computer and Information Sciences, vol. 32, no. 8, pp. 949–964, 2020.

J. Pesantez-Narvaez, M. Guillen, and M. Alcañiz, “Predicting Motor Insurance Claims Using Telematics Data-XGBoost versus Logistic Regression”, Risks, vol. 7, no. 2, 2019.

C. Tianqi and C. Guestrin, “XGBoost: A scalable tree boosting system,” in proceedings of the 22nd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining. ACM, 2016, pp. 785–94.

Downloads

Published

How to Cite

Issue

Section

License

This work is licensed under a Creative Commons Attribution-ShareAlike 4.0 International License.

All papers should be submitted electronically. All submitted manuscripts must be original work that is not under submission at another journal or under consideration for publication in another form, such as a monograph or chapter of a book. Authors of submitted papers are obligated not to submit their paper for publication elsewhere until an editorial decision is rendered on their submission. Further, authors of accepted papers are prohibited from publishing the results in other publications that appear before the paper is published in the Journal unless they receive approval for doing so from the Editor-In-Chief.

IJISAE open access articles are licensed under a Creative Commons Attribution-ShareAlike 4.0 International License. This license lets the audience to give appropriate credit, provide a link to the license, and indicate if changes were made and if they remix, transform, or build upon the material, they must distribute contributions under the same license as the original.